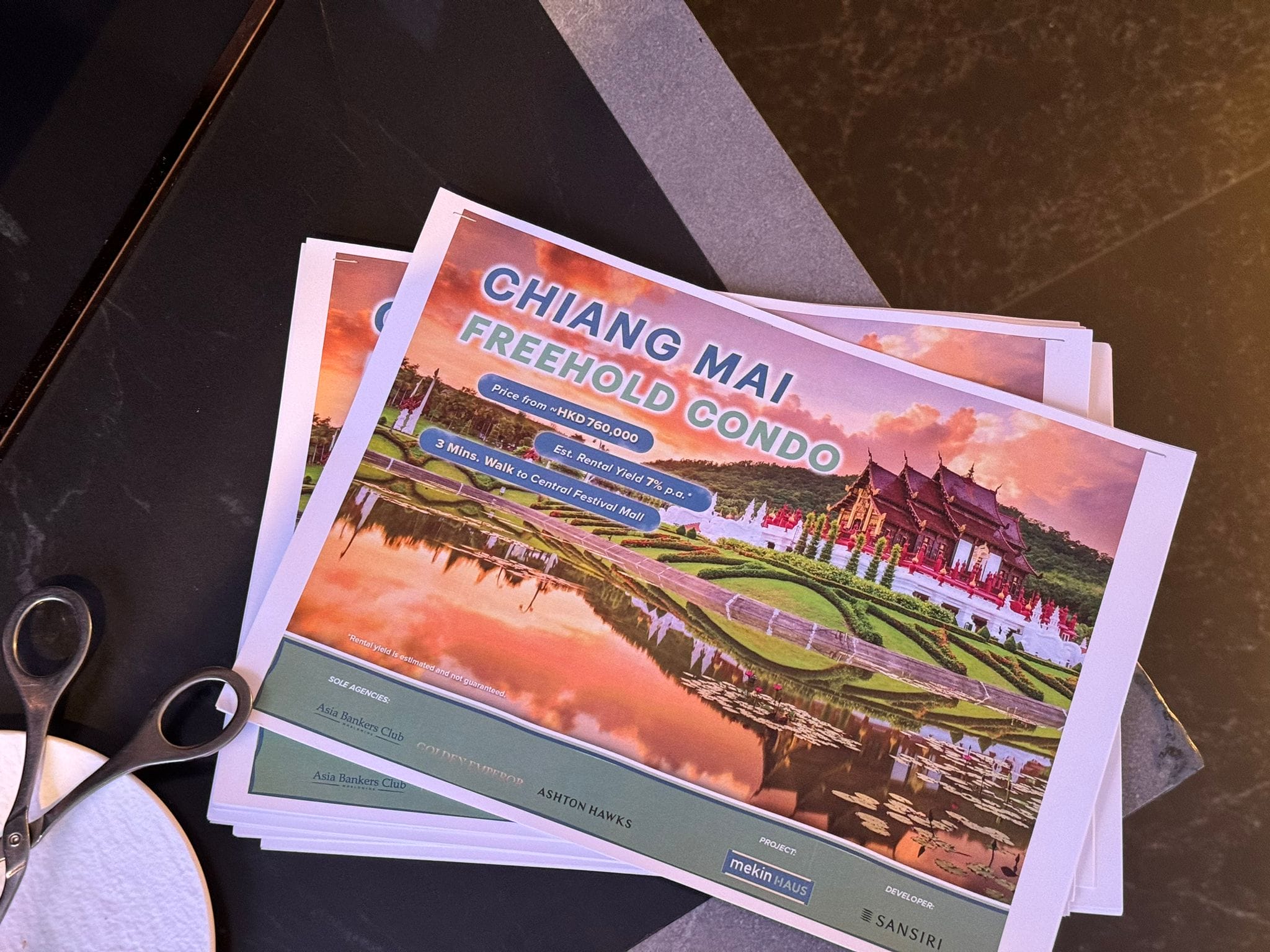

A sincere appreciation to all honorable VIPs who attended the Sansiri VIP Night last night and your presence, interest, and enthusiasm made this event tremendously successful. Brought you to the 1st pet-friendly HAUS brand in Chiang Mai by Thailand’s number 1 developer Sansiri. mekin HAUS is a boutique apartment located only a 2-minute walk from Central Festival, the largest shopping mall in Chiang Mai. The project has 30,000 square feet of resort-grade private facilities, such as a pet yard, featuring a fountained swimming pool and lush gardens, and electric vehicle charging stations, fully furnished with the high demand but limited supply. Whether you want a tranquil living environment or a convenient urban lifestyle, mekin HAUS has you covered.

Price from HKD760K and estimated 7%* return yields p.a., fully fitted and furnished upon handover and strong demand with limited supply.

If you missed the private event last night, no worries, join us this weekend for an extra 18% discount on the furniture and other items!

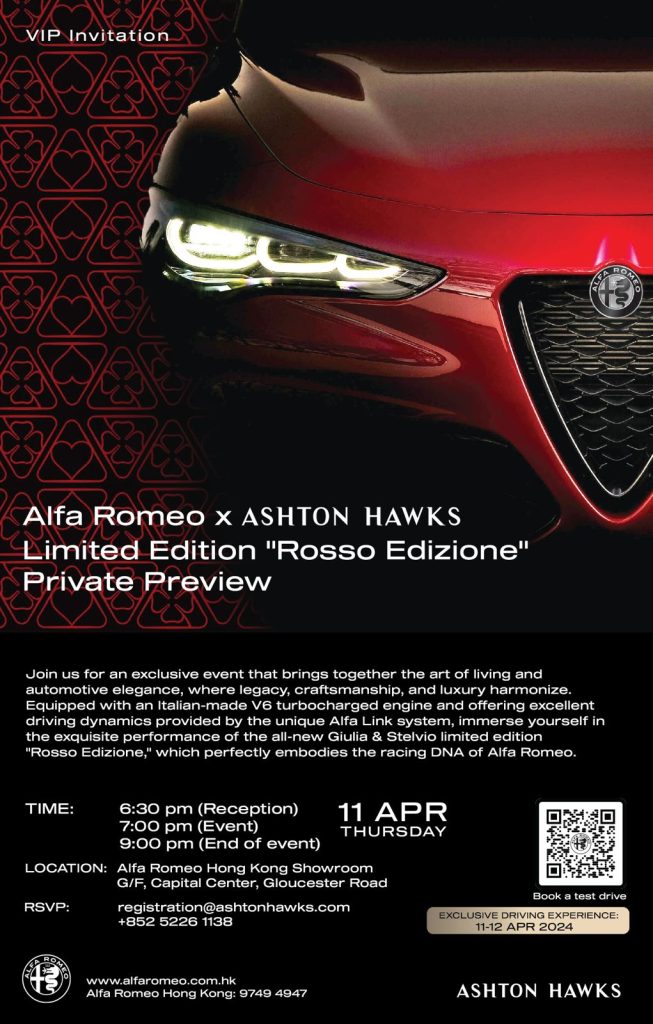

【AH Deluxe Monthly Event】Thank you to all the VIPs who joined our premium event night with Alfa Romeo, your presence made the evening truly special! We were honored to have the preview of Giulia Quadrifoglio「Rosso Edizione」& Stelvio Quadrifoglio「Rosso Edizione」. if you want to join our premium member night, please get in touch with us on

Calling all investors and property enthusiasts! Join us today for an exciting Manchester Property Truck happening across Hong Kong!

Don’t miss out on this golden opportunity to connect with Ashton Hawks’ overseas property experts, and explore the Renaker’s newest development – Contour, is a brand new 51-storey residential tower set within New Jackson – a world-class skyscraper district located at the southern gateway of Manchester city centre. With a starting price of £264K and an estimated of 7%* rental yields.

Join us today at the Manchester Property Truck across Hong Kong and unlock the doors to exceptional investment prospects.

– Feb 23: 10am Central Wellington St / 2:30pm Causeway Bay Plaza – Feb 24: 10am Tai Wai Station / 2:30pm Shatin – Feb 25: 10am TKO Park Central / 2:30pm Hang Hau Sheung Ning Rd – Feb 28: 10am One Taikoo Place / 2:30pm CWB Paterson St – Feb 29: 10am Tsun Yip St Kwun Tong / 2:30pm How Ming St Kwun Tong – Mar 1: 10am Langham Place MK / 2:30pm Haiphong Rd TST

See you there!

Manchester: Invest Now or Miss Out on Limitless Potential

【Manchester Property Investment Seminar】

Date: 2 – 3 March 2024 (SAT – SUN) Time: 12pm (ENG) | 2pm (CHI) | 4pm (CHI) Venue: 27/F, The Park Lane Hong Kong, Causeway Bay

🇦🇪 We would like to extend our heartfelt gratitude to all the VIPs who joined us on the exclusive UAE Properties Tour from November 24th to 28th. It was an incredible journey that focused on exploring the real estate offerings in the vibrant cities of Dubai and Abu Dhabi.

During this tour, we had the privilege of showcasing some of the most prestigious properties and developments in the region. From luxurious residential towers to breathtaking waterfront villas, we aimed to provide a comprehensive overview of the diverse real estate opportunities available in Dubai and Abu Dhabi. You can explore well-known projects including ready-to-move-in and off-plan projects, as well as freehold apartments, penthouses, and villas. We are honored to be a partner with ALDAR, Ellington Properties Development LLC, Emaar, DAMAC Properties, and Sobha Realty as well.

If you are interested in joining the next property tour in UAE, please contact our professional UAE experts for the next tours, we provide multilanguage services including Cantonese, English, Mandarin, Arabic, Thai, Russian, French, and German.

Invest Big Today and contact us now! (Include Golden Visa and Mortgage Consultation) Details: https://bitly.ws/34BnG WhatsApp RSVP: https://wa.link/uiiipb 📞 Enquiry | RSVP by Phone:5226 1138

——————————————————————- Want to register for the UAE All-In-One Property Investment Seminar.

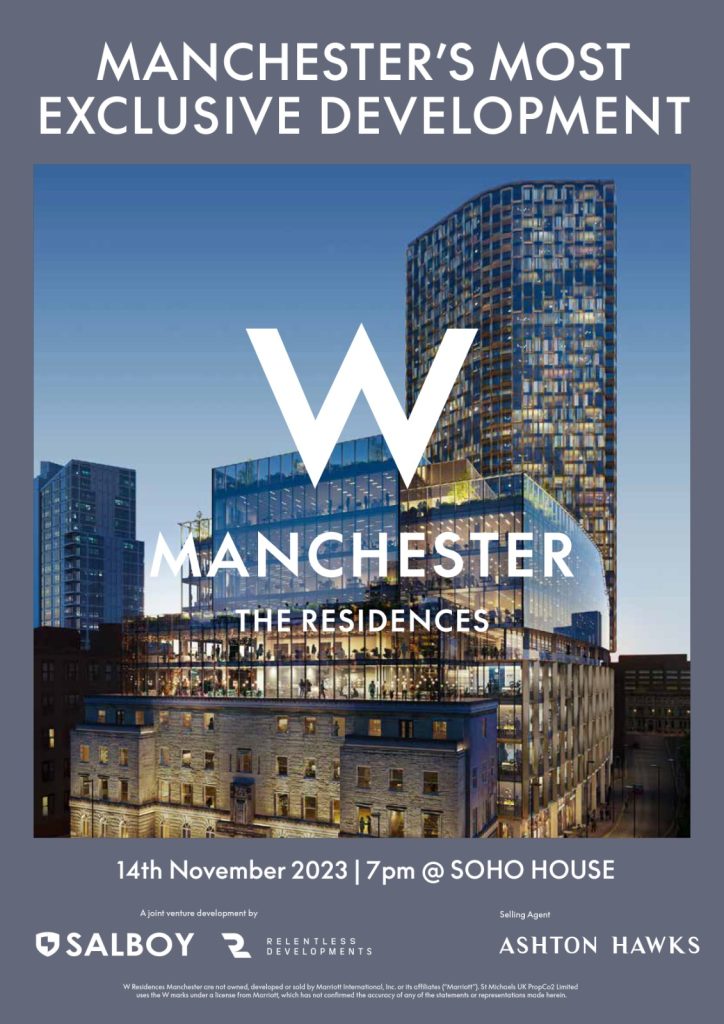

JOIN US FOR THE W RESIDENCES MANCHESTER’S SPECIAL UNITS PREVIEW

PRIME LOCATION WITH THE WORLDWIDE

AMENITIES

Proudly presents you with the prestigious residential development located in the city centre of Manchester – W Residences Manchester. Provide the world-class Marriot Standards of services with 24/7 Whatever/Whenever® Service from flight ticket bookings to transportation arrangements, ensuring a hassle-free experience. Its luxurious interior was designed by Bowler James Brindley and developed by Salboy & Relentless Developments.

【Event Details】 Date: 14 November 2023 (Tuesday) Time: 7-10 pm Venue: Soho House

Enquiry: 5226 1138 Limited seats are available. Dinner & Drinks are provided.

[Manchester’s Big News] Had a fantastic time at the media briefing held at the Salboy office!

It was an enlightening and successful event, where we had the opportunity to showcase the latest project – W Residences Manchester. The energy in the room was electrifying, as top media professionals and experts gathered to learn more about the innovative developments. A special thanks to Salboy, Relentless Developments, and all the media representatives who joined us.

Come check out Manchester’s First Branded Residences at St Michael’s on 18-19 November 2023 at the Mandarin Oriental Hotel, HK. RSVP: https://bitly.ws/ZNuR Time: 11am (Eng) | 2pm & 4pm (Canto)

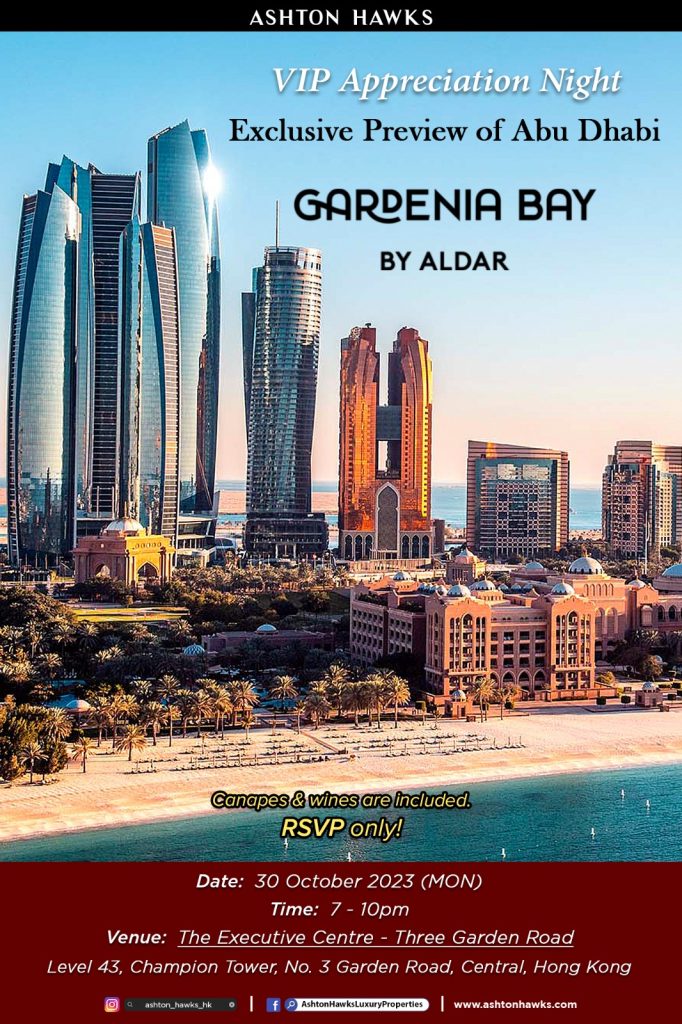

【Invest in UAE】 Thank you to all our valued guests joining the VIP Appreciation Night – Preview of Gardenia Bay By Aldar on October 30.

Amidst the bustling cityscape, Ashton Hawks proudly presents you with the 1st Hong Kong Exclusive and price list of the new home of balanced living on Yas Island, Abu Dhabi – Gardenia Bay by Aldar Phrase II. This is Aldar’s latest residential gem on Yas Island with Studios, and 1-3 Bed apartments. The development’s emphasis on green infrastructure and walkability fosters well-being and a healthy lifestyle. The thoughtful master plan maximizes shade, minimizes heat, and integrates water features, while the 10 km canal front promenade provides a vehicle-minimized environment. Picture waking up to the gentle rustle of leaves and the melodious chirping of birds, a luxury now attainable in this haven of serenity.

– Price from HKD1.7M* | Est. Rental Yield of 10%* | HKD3,300 psf. – Downpayment HKD85,000 – Up to 50% Mortgage | can flip after 20% payment – Provide Golden Visa Consultation – Freehold & Limited Overseas Quota | Limited Luxury Appliance Sets – Prime location with the best prices in the heart of Abu Dhabi – Created by the biggest Developer – Aldar Properties – Expected Handover Q3 2027 with promisingly highest quality, rental yield, and ROI for investors ——————————————————————- Want to know more about the Abu Dhabi property market? RSVP: https://bitly.ws/Ysba Date: 4-5 November 2023 (Sat-Sun) Time: 12pm (Eng) | 2pm (Canto) | 4pm (Canto) Venue:27/F, The Park Lane Hong Kong, Causeway Bay, Hong Kong Limited seats are available. By RSVP only.

【Invest in UAE】On October 25, Aldar Properties, one of the leading real estate developers in Abu Dhabi, hosted a grand and highly-anticipated event showcasing their latest and most significant property offerings. The event not only unveiled stunning properties but also provided a unique platform for property agents to explore exciting opportunities in the flourishing Abu Dhabi real estate market. Let’s dive into the highlights of this spectacular Aldar Properties event. Ashton Hawks’s agents were lucky to meet all the core members of Aldar Properties, Ms. Tracy Tutor, the famous American real estate broker and author, and Mr. Jay Shetty, the co-founder of Sama Tea.

Aldar Properties delivers exceptional properties and unparalleled investment opportunities in Abu Dhabi. From unveiling breathtaking properties to offering exclusive pre-launches and promotions, the event was a testament to Aldar’s dedication to providing innovative, sustainable, and luxurious living and working spaces.

Want to know more about the Abu Dhabi property market? RSVP:https://bitly.ws/Ysba Date: 4-5 November 2023 (Sat-Sun) Time: 12pm (Eng) | 2pm (Canto) | 4pm (Canto) Venue: 27/F, The Park Lane Hong Kong, Causeway Bay, Hong Kong Enquiry: 5226 1138 https://wa.link/rwed5v Limited seats are available. By RSVP only.

With a stable economy, business-friendly policies, and a strategic location, Dubai has become a hub for international trade and investment. From real estate to tourism, infrastructure to technology, Dubai offers a diverse range of investment opportunities that cater to the needs of investors of all kinds.

Reasons why you should not missed the Dubai market:

Geographical location

Dubai is strategically located as a gateway to Europe, Africa, and the Asia-Pacific region; making it just a short flight away from numerous countries. It is the gateway between the west and east. Dubai International Airport offers frequent flights to all major worldwide destinations, making the occasional visit home or somewhere exotic quick and hassle-free.

Stable economy

Dubai has a stable and diverse economy that is less dependent on oil than other countries in the region. The city’s government has diversified its investments into sectors like real estate, tourism, and finance, there are many job opportunities available, in a variety of industries. Dubai’s strategic location makes it an ideal hub for trade and commerce between Asia, Europe, and Africa . It is a major financial hub in the Middle East Area.

Tax-free market

Dubai is a tax-free market, there are no corporate tax, personal income tax and withholding taxes, VAT and no capital gains tax. This creates an appealing location for entrepreneurs and investors. According to the UAE Federal Law No.19 of 2018 on Foreign Direct Investment, it effectively outlines foreign ownership and under which sectors it is permitted. With zero limitations on the repatriation of profits, Dubai has a strong track record for securing foreign direct investment.

High return on investment

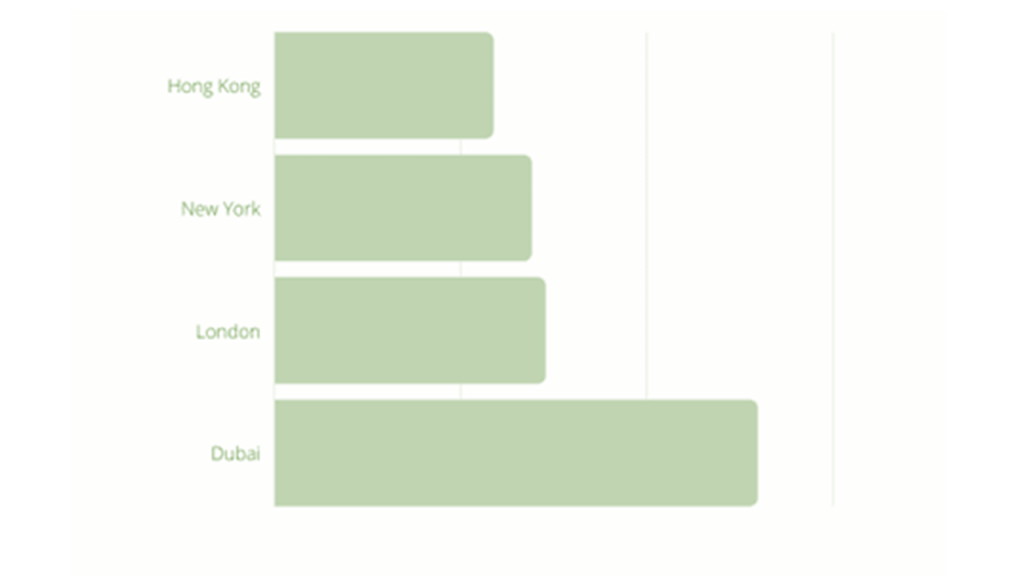

With an average yield of 9.19%, Dubai scored higher than locations such as London (7.89%) and New York (4.48%)! The city is experiencing a surge in new construction projects, which has increased demand for property and resulted in significant capital gains.

Rental Yields in Major Cities

Potential investment – Dubai’s yields outperforms other cities

Top Developers in Dubai include Emaar Properties, Sobha Realty, Deyaar, Omniyat, etc.

Areas with High Rental Yields in Dubai:

Downtown Dubai

Downtown Dubai remains a buyer’s favorite, serving as one of the world’s most visited tourist destinations. Known for its luxury high-rise towers and upscale community, it’s performing solidly in both the ready and share transfer. With more high-net-worth individuals and international executives looking to settle in Downtown, demand will continue to outstrip supply and properties will be priced at a premium in the near future. With an annualized returns for Downtown Dubai properties, it have delivered a staggering 7.90% return to our investors.

The tree-shaped Palm Jumeirah island is close to selling for USD$280 million

【Congratulation】Ashton Hawks awarded the Outstanding Overseas Property Agency Award by Hong Kong Commercial Times Business Awards 2023

Ashton Hawks has introduced different international property investment opportunities to worldwide investors, with the opening offices in Hong Kong, Vietnam, and Thailand to support the growing need for sourcing and managing real estate investment portfolios for valued clients.

This year, Ashton Hawks is honored to be awarded the Outstanding Overseas Property Agency Award by Hong Kong Commercial Times Business Awards 2023 in September 2023. It is highly professional and recognized in the overseas property market. Thanks again to HKCT for their affirmation and support to us. This is a great honor and encouragement for us. We will continue to work hard to provide customers with more high-quality international properties and our professional services.

The winners of <HKCT Business Awards 2023> are based on the four judging criteria of enterprise growth + market competition + brand concept + professional positioning. About the HKCT Business Awards 2023 1. Official award website: https://hkct-awards.com/articles/59 2. Official Facebook: https://www.facebook.com/hkct.asia 3. Judged by an independent jury composed of several industry experts from HKCT. 4. Judging focuses on quality, service, innovation, originality, and commitment to sustainability as overarching themes.

Ashton Hawks will search for the most suitable overseas high-quality properties for you. If you have any inquiries about properties investment, rental management, and mortgage consultation, please https://wa.link/1klpcb